PhD Workshop

This workshop offers doctoral students within the RU a dedicated platform to present their research and receive feedback from faculty and peers. It provides an opportunity for young scholars to refine their ideas, improve their methodologies, and develop their academic networks. The event fosters a supportive research environment, encouraging collaboration between PhD students and senior researchers. By engaging with the broader research community, participants gain valuable insights that enhance their work. The workshop strengthens the training and development of the next generation of scholars in intermediary asset pricing.

PhD Workshop 2025

The PhD Workshop on Intermediary Asset Pricing took place on May 8–9, 2025, at KIT in Karlsruhe. This two-day event offered a mix of research presentations and professional development, bringing together PhD students across the Research Unit.

The first day was dedicated to presentation skills, led by communication coach Francesca Carlin. Through a combination of short talks by all participants and focused feedback sessions, the workshop aimed to enhance academic communication. Participants also discussed storytelling in research.

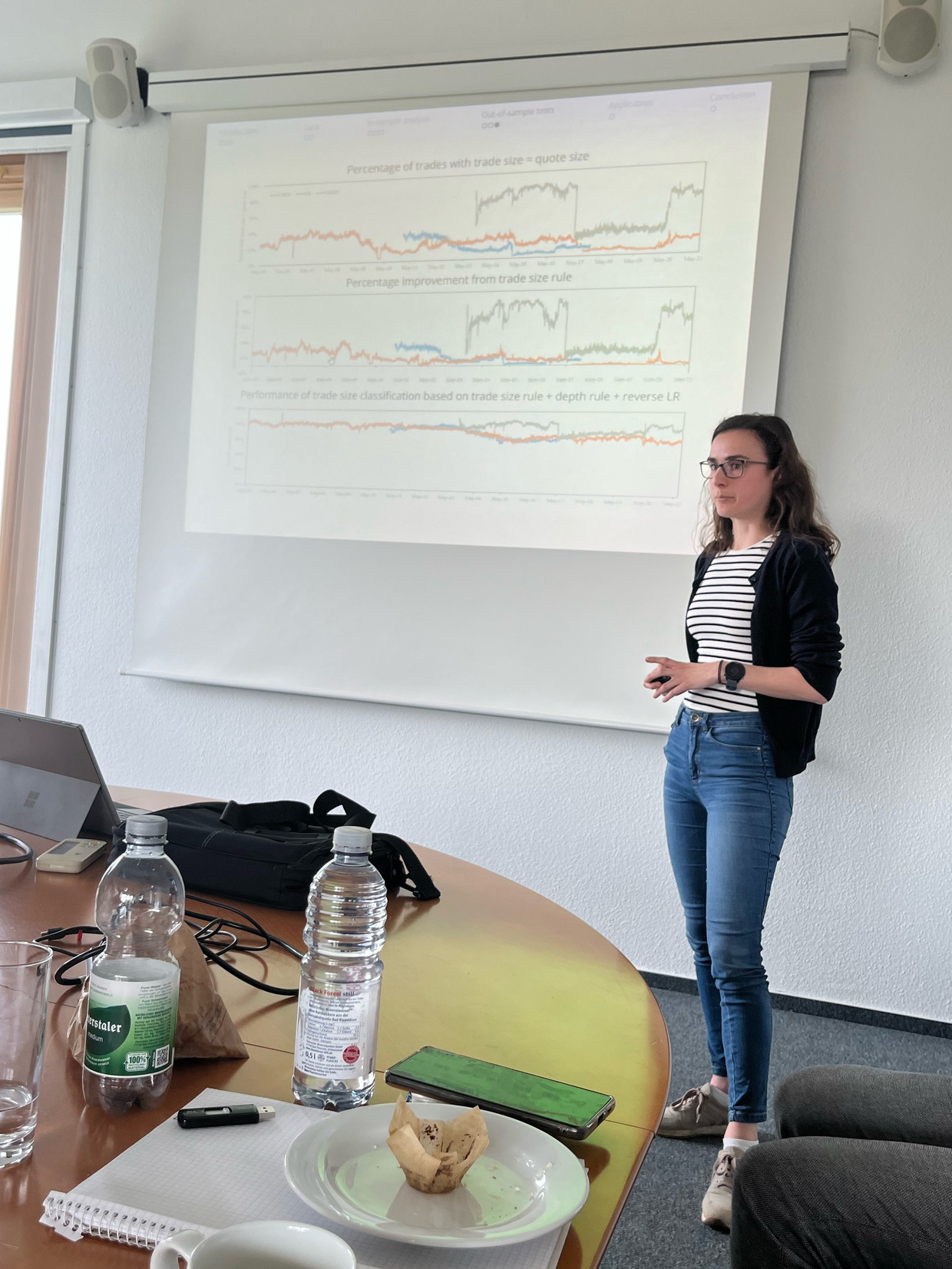

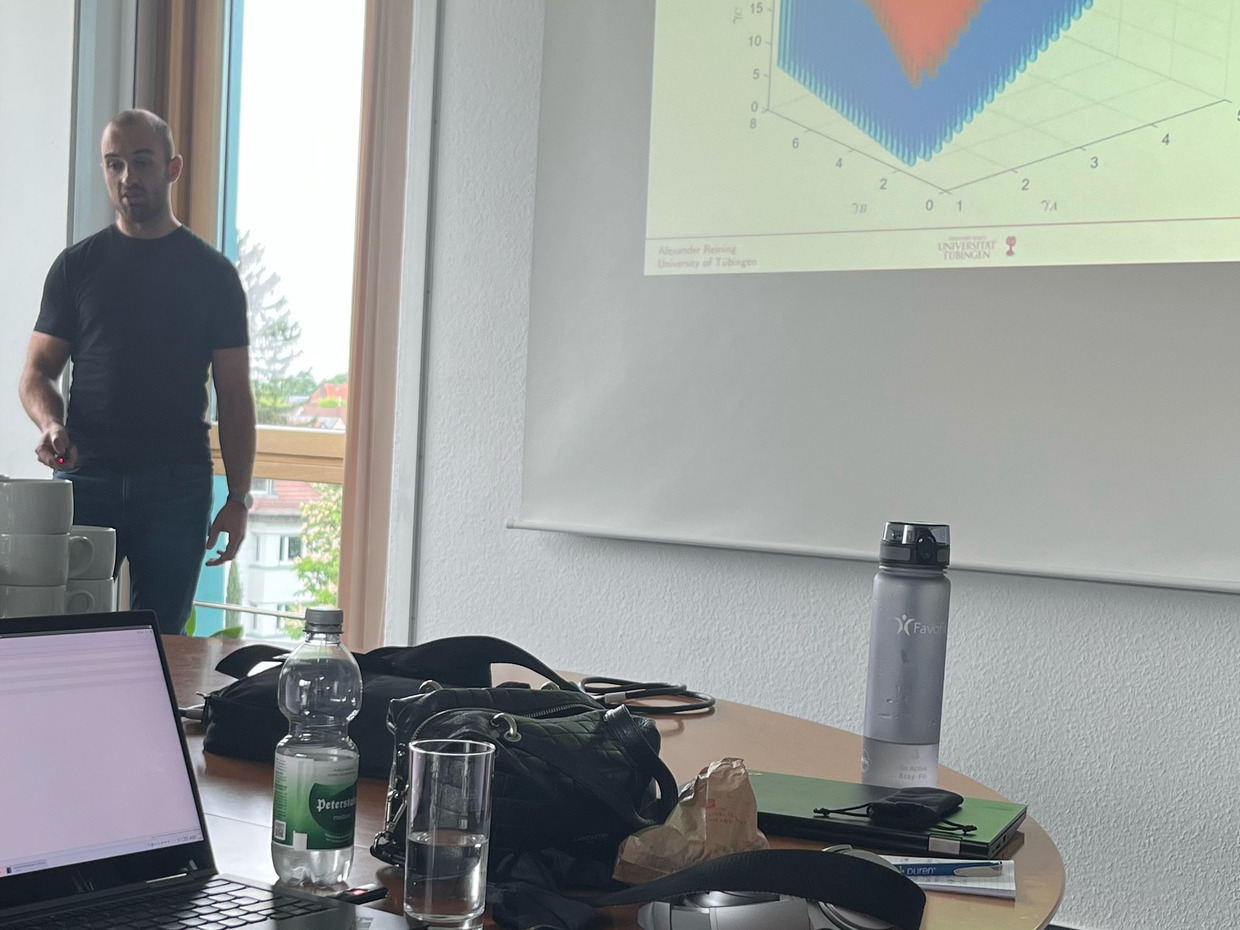

On the second day, selected researchers presented their ongoing work in greater depth. Alexander Götz, Alexander Reining, and Fanchen Meng each delivered extended presentations on their respective projects, followed by constructive group discussions. The workshop fostered both academic exchange and personal development, offering a supportive environment to refine both research ideas and presentation techniques.

PhD Workshop 2024

The PhD Workshop on Intermediary Asset Pricing was held on May 8, 2024, at KIT, Karlsruhe. The workshop brought together PhD students and senior researchers for a series of presentations and discussions. You can find the program here.

Leonie Wieneke kicked off the day with a presentation on Project B01, followed by Jan Harren who presented on Project A22. David Worms then shared his work on Project A21, and Johannes Dinger presented on Project A12.

The afternoon session began with Tom Ernst presenting on Project A14, with a discussion led by Patrick Brock. Franziska Weishaupt followed with her research on Project A12, with Leonardo Minoia serving as the discussant. After a coffee break, Fanchen Meng presented on Project A23, with Marius Schmidt providing the discussion.

The day concluded with Philipp Höfler presenting on Project A13, providing a great opportunity for interaction and feedback among the participants.

PhD Workshop 2023

The PhD Workshop on Intermediary Asset Pricing took place on May 11, 2023, at KIT, Karlsruhe. The event featured presentations by PhD students on their research projects, followed by discussions with senior researchers and peers. You can find the program here.

Matthias Molnar presented his work on Project A22. Alexander Reining followed with insights into Project B02. Leonie Wieneke presented on Project B01 shortly after, discussing her research. The day included a session on Women in Finance, which highlighted the role of women in the finance industry.

In the afternoon, Julian Böll presented on Project A23, with a discussion led by Philipp Höfler. Jan Harren then shared his work on Project B01. Finally, Caroline Grauer presented on Project A22, with Patrick Rank serving as the discussant. The event provided a great opportunity for students to showcase their work and engage in meaningful discussions with peers and senior researchers.

PhD Workshop 2022

The PhD Workshop was held on May 12, 2022, at KIT, Karlsruhe. During the workshop, PhD students presented their own research in front of senior researchers and fellow PhD students. You can find the programm here.

Matthias Molnar presented on "Understanding Biases in Option Returns", discussing the biases influencing option returns in financial markets. Caroline Grauer followed with a presentation on "Option Trade Classification", focusing on methods for classifying option trades in market data. Julian Böll concluded the presentations with his research on "Anomalies across Optionable Stocks", exploring patterns and anomalies in stocks with option availability. The event also featured a welcome and introductory session, followed by a science walk for networking. The day ended with an apéritif and dinner at Gasthaus Gutenberg.