Models & Methods Workshop

These workshops focus on the development and refinement of models and empirical methods relevant to intermediary asset pricing. They provide a dedicated space for researchers to discuss methodological challenges and coordinate their approaches. By fostering methodological innovation, the workshops enhance the quality and consistency of research outputs. They also help integrate theoretical and empirical advancements within the RU.

Models & Methods Workshop 2026

On February 19 and 20, 2026, the research group’s annual M&M workshop took place at KIT in Karlsruhe. Once again, the workshop provided a valuable platform for discussing methodological approaches and exchanging views on the current status of research in the subprojects. The program can be found here.

The first day began with a presentation of subproject A12, in which Franziska Weishaupt presented her work on the fragility of corporate bonds. This was followed by a presentation from subproject A22 on research into liquidity premiums in the options market, presented by Caroline Grauer, Alexander Götz, and Mathias Molnar. After the coffee break, there was a presentation from project A14, in which Tom Ernst examined the role of passive funds in the context of intermediary asset pricing theory. The day concluded with a meeting of the project leaders and a group dinner.

On the second day, Leonie Wieneke opened with a presentation from Project B01 on heterogeneous investors and habit formation. Fanchen Meng then presented current research from Project A23 on estimating structural shocks using sign-restricted VAR models. The session concluded with a presentation by Rüdiger Weber from Project A15 on applications and further developments of demand-based asset pricing models. The event concluded with a joint lunch and provided numerous opportunities for productive discussions as well as for deepening existing and future collaborations within the research group.

M&M Workshop 2025

On February 13–14, 2025, the Research Unit held its annual Methods & Modelling Workshop at KIT in Karlsruhe. The workshop provided a valuable forum for deepening methodological foundations and discussing ongoing research across subprojects. You can find the program here.

The first day focused on demand-based asset pricing, with presentations by Patrick Brock and Rüdiger Weber, followed by a session from A12 on the distinct risk profile of corporate bond ETFs, presented by Johannes Dinger. The day concluded with a project leader meeting and a joint dinner.

The second day featured contributions from B01, where Leonie Wieneke explored heterogeneous investors in a production economy. The event closed with a farewell session, fostering productive discussions and future collaboration within the RU.

M&M Workshop 2024

On May 13, 2022, the DFG Research Unit FOR 5230 held its Methods & Modelling Workshop at KIT, in Karlsruhe. The workshop focused on foundational and advanced modeling techniques relevant to intermediary asset pricing. Participants explored theoretical frameworks, numerical methods, and model applications, aiming to refine analytical tools used in financial market research. The event provided an opportunity for in-depth discussions on model structures and methodological advancements. You can find the program here.

The workshop began with a session on the baseline model of He & Krishnamurthy (2013), setting the stage for later discussions. The afternoon sessions focused on numerical methods, Epstein-Zin utility functions, and long-run risk models, providing insights into their implementation and relevance for intermediary asset pricing. The final session explored production-based asset pricing models. The workshop fostered an engaging exchange of ideas, strengthening methodological expertise within the research group.

_rdax_1240x930s.jpg)

_rdax_1240x930s.jpg)

_rdax_1240x930s.jpg)

_rdax_1240x930s.jpg)

M&M Workshop 2023

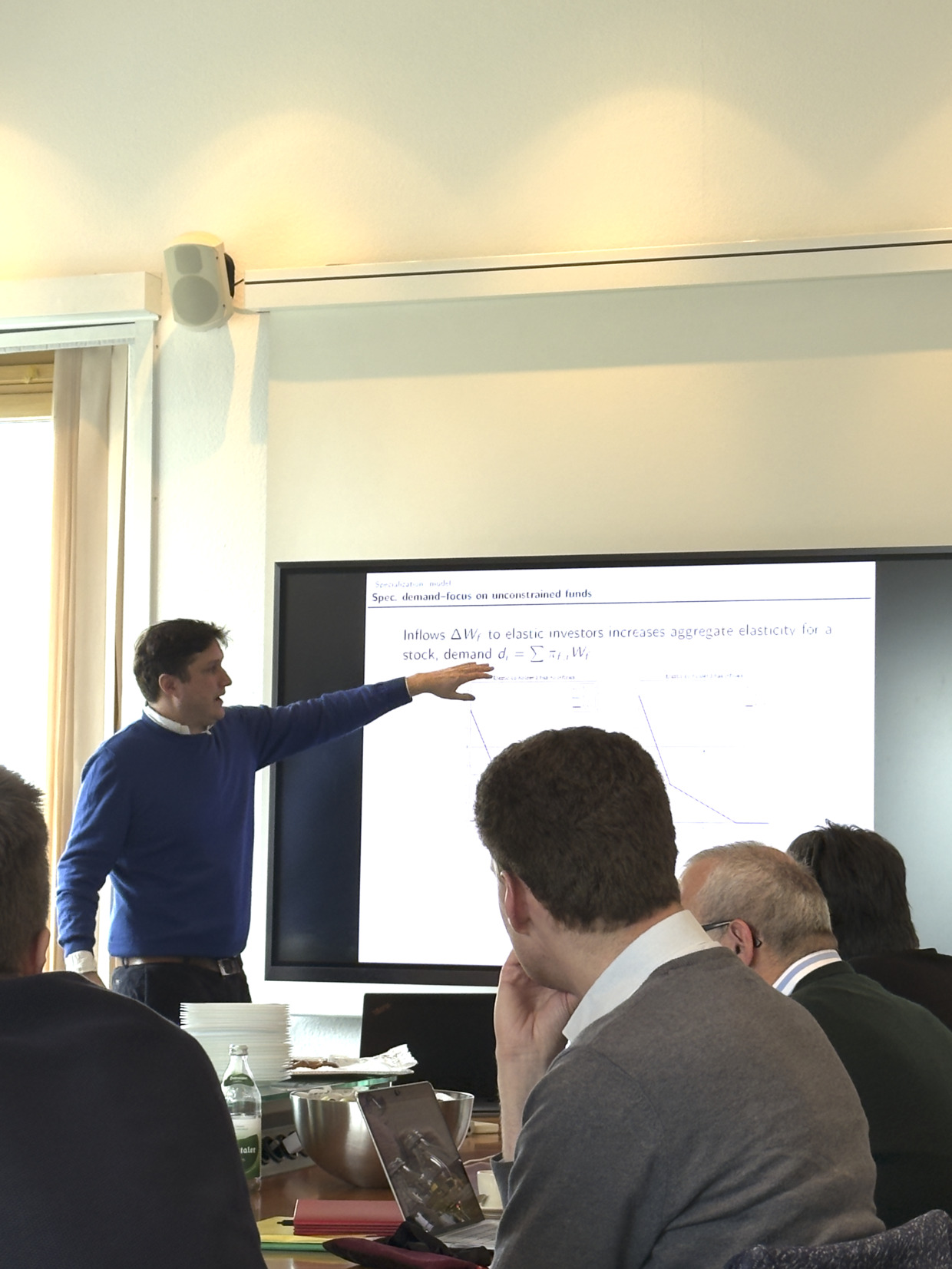

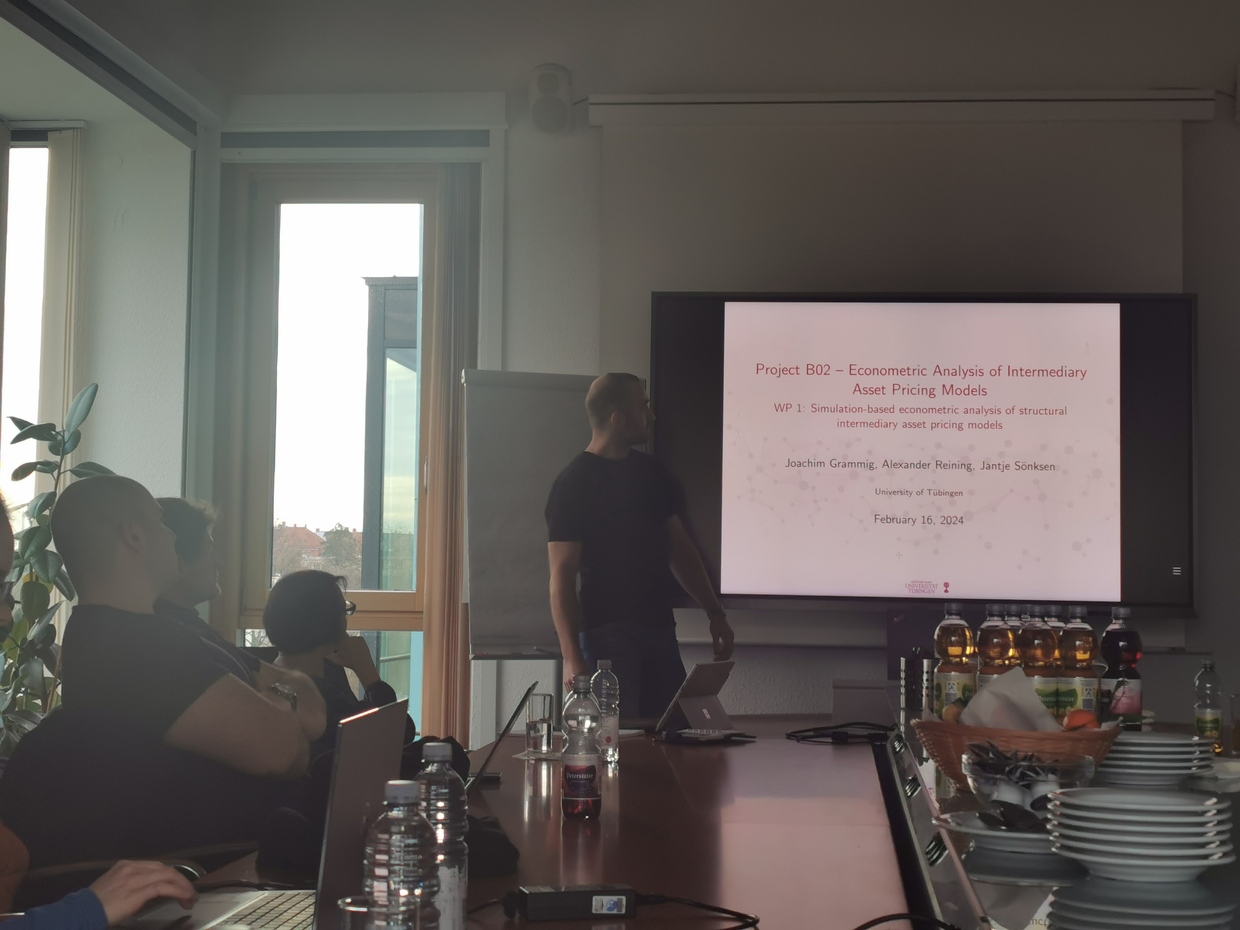

On February 23–24, 2023, the Research Unit hosted its Methods & Modelling Workshop at KIT, in Karlsruhe. The event focused on the theoretical models used by each of the subprojects within the research group. Several projects presented its modeling approaches and methodologies in the context of intermediary asset pricing, facilitating valuable discussions among participants. This workshop provided an opportunity to refine models and approaches, contributing to the overall progress of the research unit. You can find the program here.

Throughout the two days, A14, A23, B01, A12, and B02 presented their theoretical models, focusing on different aspects of intermediary asset pricing. The presentations fostered constructive discussions, with participants providing valuable feedback on the models and suggesting new avenues for future research. The workshop also featured informal discussions over meals, including a dinner at Kaisergarten, which enhanced the exchange of ideas among the researchers. The event concluded with a farewell lunch, leaving participants with fresh insights and a strengthened sense of collaboration within the group.

M&M Workshop 2022

On May 13, 2022, the DFG Research Unit FOR 5230 held its Methods & Modelling Workshop at KIT, in Karlsruhe. The workshop focused on foundational and advanced modeling techniques relevant to intermediary asset pricing. Participants explored theoretical frameworks, numerical methods, and model applications, aiming to refine analytical tools used in financial market research. The event provided an opportunity for in-depth discussions on model structures and methodological advancements. You can find the program here.

The workshop began with a session on the baseline model of He & Krishnamurthy (2013), setting the stage for later discussions. The afternoon sessions focused on numerical methods, Epstein-Zin utility functions, and long-run risk models, providing insights into their implementation and relevance for intermediary asset pricing. The final session explored production-based asset pricing models. The workshop fostered an engaging exchange of ideas, strengthening methodological expertise within the research group.

_rdax_1240x825s.jpg)

_rdax_1240x825s.jpg)

_rdax_1240x826s.jpg)

_rdax_1240x825s.jpg)